Income-generating expenses are deductible from the gross rent such as interest expense cost of repairs assessment tax quit rent and agents commission. 1 The property is jointly owned by husband and wife but then taxed separately 50 upon each partner.

How To Calculate Germany S Per Diem Rates In 2022

In order to promote affordable accommodation to the.

. 2 Exchange rate used. Due to the decrease of income from rental business income from the holding of investment is more than 80 of the. In Budget 2018 the government introduced a new limited time tax exemption designed to control home rental prices.

For instance they include. B is the gross income consisting of dividend interest and rent chargeable to tax for that basis period. Now in 2019 the time has come for property owners to begin claiming that exemption on their income tax forms.

So to reiterate only your net rental income will be taxed. As of 1st January 2020 LHDN has announced that property rental in Malaysia is taxed at 24 and property rental income is calculated on a net basis. In other words if the rental source is ongoing or continuing expenses for the entire basis period are deductible even if there may be periods when no rental income is produced due to temporary vacancy.

Payment for accommodation at premises registered with the Commissioner of Tourism and entrance fee to a tourist attraction expenses incurred on or after 1 March 2020 until 31 December 2021 1000. Depreciation does not qualify for tax deductions. Payment for accommodation at premises registered with the Commissioner of Tourism and entrance fee to a tourist attraction expenses incurred on or after 1 March 2020 until 31 December 2021 1000.

Expenses claimed are as follows. Amount RM Individual chargeable income less than RM35000. Firms and associations are permitted to use the Public Ruling for training purposes only.

3PROHIBITED EXPENSES Expenses not wholly and exclusively incurred in the production of income Domestic private or capital expenditure The Company can claim capital allowance for capital expenditure incurred Lease rentals for passenger cars exceeding RM50000 or RM100000 per car the latter amount being applicable to. Rental income is taxed at a flat rate of 24. Depending on the tenant the prestige of the area may or may not be of importance.

Before declaring your rental income to LHDN you should start from the rental income sources. Prior to Jan 1 2018 all rental income was assessed on a progressive tax rate ranging from 0 to 28 without any tax incentive or exemption. Income-generating expenses such as quit rent assessment repairs and maintenance fire insurance service charge sinking fund and management fees are deductible.

A is the total of the permitted expenses incurred for that basis period reduced by any receipt of a similar kind. The idea is that income from the renting of residential properties would receive a 50 exemption from income tax. And C is the aggregate of the gross income consisting of dividend whether exempt or not interest and rent and.

100 US 400 MYR. Nonresidents are taxed at a flat rate of 24 on their Malaysian-sourced income. If you had received RM24000 as rental income in one year but you spent RM26000 on permitted expenses this would be considered as a loss and you wont have to declare that RM24000 as rental.

Net basis calculation is based on the finalised earning after the deduction of direct expenses like assessments quit rent upkeeps and repairs. It can be derived from immovable properties and movable properties. To refer more info about Malaysia taxation on rental income please refer Public Ruling 1 of 2004 Income of letting real property as below.

Expenses claimed RM Directors fees 24 Salaries and allowances 16 Management fees 5 Audit fees 4 The amount of A B dan C are as follows. Suria Property Sdn Bhd is an IHC based on its main activity and the income from holding of investment that exceeds 80 of the companys income. A business that wishes to give a good impression to their clients may want to search for a more prestigious address while higher-ranking personnel looking for a home to rent may want a unit in a more prestigious area.

The Rules provide that in ascertaining a companys adjusted income from its business for a YA a further deduction ie deduction in addition to any deduction allowable under Section 33 of the ITA shall be allowed for the expenses incurred by the company for the rental of premises for its employees accommodation between 1 January 2021. Other instances of permitted expenses would be insurance and quit rentmaintenance. Systemic or multiple reproduction.

Amount RM Individual chargeable income less than RM35000. 31 Resident means resident in Malaysia as determined under paragraphs 81b and 81.

You Made A Mistake On Your Tax Return Now What

Average Cost Of Credit Card Processing Fees Bankrate

How To Calculate Rental Income Tax Net Profit Towergate

Can You Write Off Theft On Taxes Not Anymore

Contractor Overhead And Average Profit Margin In Construction

19 Payment Voucher Templates Free Printable Word Excel Pdf Formats Samples Designs Layout Voucher Template Free Word Template Templates Printable Free

Capital Expenditure Vs Repairs And Maintenance Keyrenter Denver

Accelerating Tax Deductions For Prepaid Expenses Windes

:max_bytes(150000):strip_icc()/dotdash-INV-final-Absorption-Costing-May-2021-01-bcb4092dc6044f51b926837f0a9086a6.jpg)

Absorption Costing Definition

Like Kind Exchanges To Be Limited Under Biden S Tax Proposals

2021 Major Tax Breaks For Taxpayers Over Age 65

Key International Property Tax Filing Tips For Non Resident Airbnb Hosts

What Happens If I Don T File Taxes Turbotax Tax Tips Videos

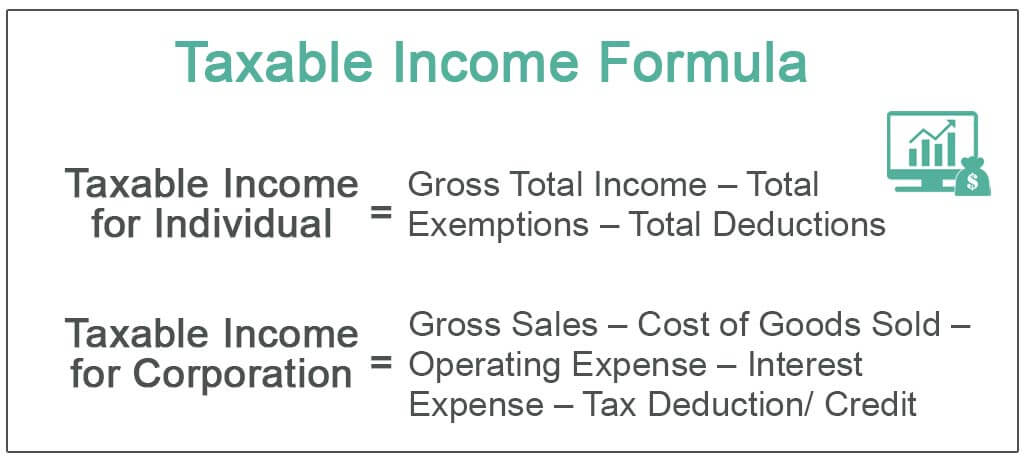

Taxable Income Formula Examples How To Calculate Taxable Income

5 Free Sample Of Certificate Of Ownership Form Template Certificate Templates Business Template Free Certificate Templates

Key International Property Tax Filing Tips For Non Resident Airbnb Hosts

Landlord Tax Guide Paying Tax On Your Rental Income Bollington Insurance Bollington Insurance Brokers

Property Management Company Denver Co Walters Company

Enter The World S Greatest Work Trip From Caterpillar Cat Caterpillar